Beyond the Magnificent Seven: Investment Lessons from America's Economic Playbook

#6 – February 2025 – 02/24/2025

This newsletter is for informational purposes only and is not intended to be financial advice.

Macro Insights

United States

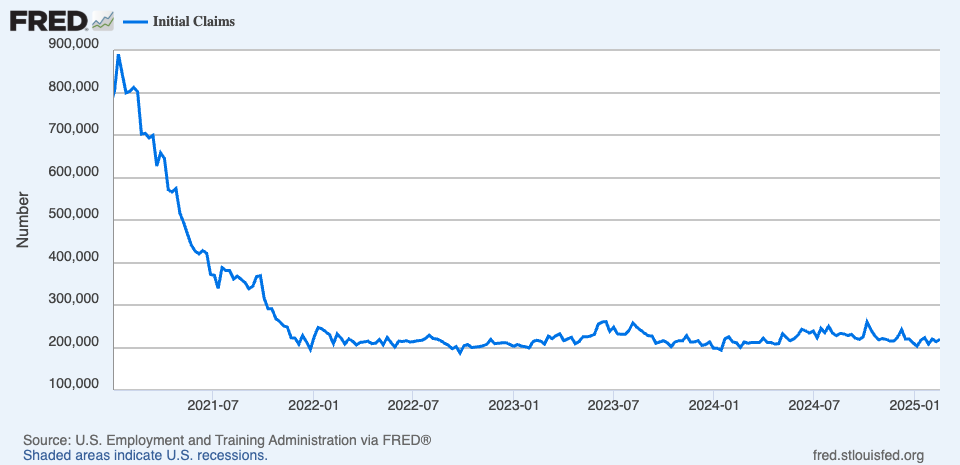

The probability of the Fed cutting interest rates in a few weeks is less than 5%, as the US economy continues to outperform its peers week in and week out. This week, both initial jobless claims and continued claims rose slightly, while still at stable and decreasing levels over the longer-term. Initial claims came in at 219,000 – rising by 4,000, while continued jobless claims were 1,869,000 – 24,000 higher than last week. The unemployment rate in January dropped rather unexpectedly to 4% from 4.1%, while the participation rate edged higher to 62.6%. Average hourly earnings also unexpectedly held steady at 4.1%, as estimates for earnings growth were 3.8%. Finally, average weekly hours worked fell by 0.1 hours to 34.1. As we continue to monitor both sides of the Fed’s mandate, the employment side continues to remain quite healthy.

Looking at the inflation side of their mandate further solidifies the narrative that the Fed will hold off on cutting rates at their next meeting, and maybe even for quite some time. Last week’s inflation report showed that both headline and core inflation rose unexpectedly, with headline inflation now at 3% (up from 2.9%) and core inflation at 3.3% (up from 3.2%). The latest consumer inflation survey performed by the University of Michigan, now shows that consumers feel higher inflation is engrained into the economy, with 5-year inflation expectations now at 3.5%, and inflation expectations over the next 12 months rising to 4.3% - the highest since 2023. After its release, the consumer survey by the University of Michigan led U.S. markets to post a significant drop on Friday.

Producer prices also came in higher than expected, with headline PPI rising 3.5% YoY and 0.4% MoM. Core PPI was even higher, at 3.6% YoY. With still elevated producer prices, there is concern that those higher prices will be passed down to the consumer and show up in CPI.

Although inflation is still elevated, there’s a chance that in the coming months it may recede. In the early months of 2024, inflation was climbing at quite a fast pace, something that’s still affecting current inflation data, a phenomenon known as the base year effect. It’ll be a few more months before that drops off, and, holding all else constant, inflation might subside a bit.

While inflation remains above target, an advance estimate of January retail sales showed that consumers bought less than they did in December. Grocery store, gas station, department store, miscellaneous stores and food services and drinking places were the only sectors that saw their sales grow that month. The largest decreases in sales came from motor vehicles, sporting goods, hobby, musical instrument and bookstores, and non-store retailers. Some of that decrease could be due to seasonality, as January isn’t usually a great month for selling cars. While retail sales dropped, the month-to-month change in January was still better than it was for the same month the year before. Last month, retail sales excluding autos dropped 0.4% on a month-to-month basis, while the same figure for the month of January 2024, showed that retail sales excluding autos fell o.8%. So, while headlines emphasised that retail sales had dropped last month, they’re still relatively solid, rising 4.2% in January on a year-over-year basis.

The yield on 10-year government bonds has also been dropping from its high in January – around 4.8%. It’s hovering around 4.43% as of this weekend. With inflation still elevated, I think yields have been falling mainly because investors believe that Elon Musk’s DOGE efforts are starting to, and will continue to, pay off. If deficits indeed fall, this will be a very bullish sign for government bonds as high yields have been pricing in the risk of debt monetization – diluting the real value of those bonds.

Finally, January ISM reports showed that manufacturing in the US expanded for the first month in over 2 years. Most likely in response to Trump’s signalling of efforts to bring more manufacturing jobs back to the U.S. The ISM new orders index has also been expanding for the past three months. Economic activity in the services sector is also expanding, and has been for over half a year now.

While the economy has been hot recently, there are still significant risks present, the biggest of which is geopolitical tensions. The risk of broad tariffs could trigger trade and supply shocks. Other risks also continue to be apparent, such as the path of interest rates and a slowdown in AI enthusiasm. Two of the main catalysts for the recent rally in equities have been the Fed cutting rates and the AI craze. With rate cuts no longer imminent, U.S. equities may face some headwinds. There’s also the question of what’s next for AI, and how that plays out will be sure to drive markets over the near term.

Europe and Canada

Over the last little while, the term American exceptionalism has become commonplace. In the past 10 years, U.S. markets have outperformed most of the developed world. The S&P 500 had a return of 246%, while German markets had a return of 59%, the UK had returns of 43% and the highest returns in Europe, found in France, were 97%. Around the world, the story is the same, Canada saw a 10-year return of 87.9%, Japan – 71.9%, Australia – 70.2% and China – 26.2%.

So why has the United States outperformed so immensely?

Although there’s probably a lot of answers to that question, I think the most important answers to that question are productivity, innovation and investment. The US has been a productivity machine, and a place where innovation thrives, but what caused that innovation and productivity growth? I think one of the biggest causes of their outperformance in innovation and productivity, is investment. To have growth and innovation you first need to invest in it, whether that’s time, money, skills or other resources – all of which America has in abundance.

One key difference that I see in America versus other major economies is the way the general public invests. The American population places a strong emphasis on investing in stocks, especially domestics stocks – tying much of their own wealth to the wealth of the country as a whole. According to a recent poll by Gallup, 62% of adult Americans invest in stocks. In Canada, that figure is 47%, and in Europe it’s even lower – between 18%-28%. In November, Stu Kedwell (Managing Director – RBC Global Asset Management) said, “So even amongst Canadians, where there has been some enthusiasm, it's normally been for US stocks”. Even out of that 47% of Canadians that invest in stocks, the number of people that invest in Canadian stocks is even smaller. This is bad for multiple reasons, but most importantly because capital is not flowing to the most productive domestic sources that will grow the economy. This is part of what makes U.S. capital markets so efficient – because capital is flowing from those that don’t need money right now to those who do need it and will use it in the most productive way. Just look at the GDP per capita of the U.S. (shown in blue below) compared with the UK, Europe and Canada over the past ten years and you’ll see there is a real difference between productivity in America compared with other countries.

What I think America is doing right, and what other countries should look to emulate is how they invest in productivity and how they manage personal finances. An example of this is the comparison between Canada and America – neighbours but very different in their approach to investing. Over the past decade or so, Canadians took on larger amounts of credit relative to incomes, which created buying power in the past, and which I think is now reducing their buying power in the present. American household debt service payments in relation to their income were ~11.3% in the 3rd quarter of 2024, while Canadians spent ~14.7% of their income to service their debt. For someone making the median Canadian income, that’s roughly an extra $2,400 a year going towards debt. Rather than using that credit to invest in the productive capacity of the economy, through innovating and creating businesses that produce products and services to sell to other countries, Canadians used a large chunk of it to purchase housing and real estate. In Canada, as of 2022, 30% of Canadian homes were owned by individuals who own multiple properties, and a little over half of the country’s net worth was held in the value of real estate. As of March 2024, Canadians also had the highest household debt to disposable income ratio of all G7 countries. In America, about only 10% of homes were owned by individuals who own more than one home, and around 22% of American’s net worth is in the value of real estate.

Over the past decade or so, through the creation of large amounts of credit and lots of demand for real estate, Canadians continued to pursue what they thought was a winning strategy. Now we are seeing that strategy is causing tremendous difficulty for the economy. Productivity has been dropping because of a lack of investment, and GDP has also been stagnant – in part because Canadian consumers are stretched thin and are now in the phase of paying back what they borrowed a while ago. Debt always causes cycles in the economy. When debt is being created, it causes the economy to boom because people have lots of purchasing power, but when they use up that purchasing power and it comes time to pay back that debt, it leads to a reduction in the amount that people can consume and spend.

In contrast, the American population, places a much larger emphasis on investing in the stocks of companies that are breeding innovation and helping to grow the economy. In the most recent letter Warren Buffet wrote to Berkshire’s shareholders, he touched on this, saying:

“One way or another, the sensible – better yet imaginative – deployment of savings by citizens is required to propel an ever-growing societal output of desired goods and services. This system is called capitalism. It has its faults and abuses – in certain respects more egregious now than ever – but it also can work wonders unmatched by other economic systems.”

This is a lesson that people in countries outside the U.S. need to look closely at and replicate. To increase productivity and grow the economy, populations need to invest in new ventures, businesses and building products and services, within their own economy that will provide value to people elsewhere. To understand this, just look at some of the largest companies in the world – household names like Apple, Amazon, Google and Facebook. These are companies that have created products and services that over half the world uses.

Another important consideration in the productivity equation is the talent that America has been able to attract. I think we are now seeing a snowballing effect in other countries, where the conditions needed for businesses and innovation to flourish are continuing to deteriorate. When you have low levels of innovation, like in Europe, Canada and other countries, they have difficulty attracting talented individuals, and end up losing the talent they do have because there isn’t enough supply of jobs for those individuals at their skill levels. When talent leaves the economy for a more attractive one, this leaves those countries with a workforce that doesn’t prioritize innovation. In turn, this causes the economy to fall shy of growing businesses relative to the rest of the world and ultimately leads back to the original problem – a loss of talent due to a lack of innovation. This continues in a loop until what’s left is a less motivated workforce, and a challenge for leaders to motivate workers to be productive. For leaders to stay elected, they generally have to give voters what they want – which are benefits that don’t align with the goal of increasing productivity, and so the cycle continues to spiral.

In many countries urgent change is needed, and governments need to incentivize and reward innovation, and risk-taking rather than trying to stifle it. For example, Canada’s decision to increase the capital gains inclusion rate, does the opposite, by disincentivizing people to create and take risks through lowering their reward. Although it looks increasingly likely that this tax proposal will not come to fruition, it is just another one of the decisions that Canadian lawmakers are making that will cause productivity to fall in the long run.

On another note, this past Tuesday, Statistics Canada released January’s inflation report in which inflation rose at a faster than expected pace. Headline inflation rose 1.9%, and measures of core inflation, removing more volatile components, CPI-median and CPI-trim, both rose at a pace of 2.7%. Although headline inflation was just under the Bank of Canada’s target, part of that was due to temporary GST/HST tax breaks, which caused the price of components such as food, alcoholic beverages, toys, games and hobby supplies to fall. The effects of these tax breaks will continue to affect the data until February, and it’ll be interesting to see whether inflation continues to rise, possibly holding the BoC back from cutting rates further. Finally, the latest Canadian retail sales report showed that retail sales jumped fairly dramatically, up 3.9% YoY and 2.5% MoM. This could give the BoC even more reason not to cut rates, and evidence that the monetary policy may not be as contractionary as it once was.

Equities

While researching and trying to pinpoint a specific stock to touch on in this edition, I found myself not being able to reach the point where my conviction was strong enough on any specific stock. Instead, I thought I would share some of the themes that I am seeing across equity markets as a whole.

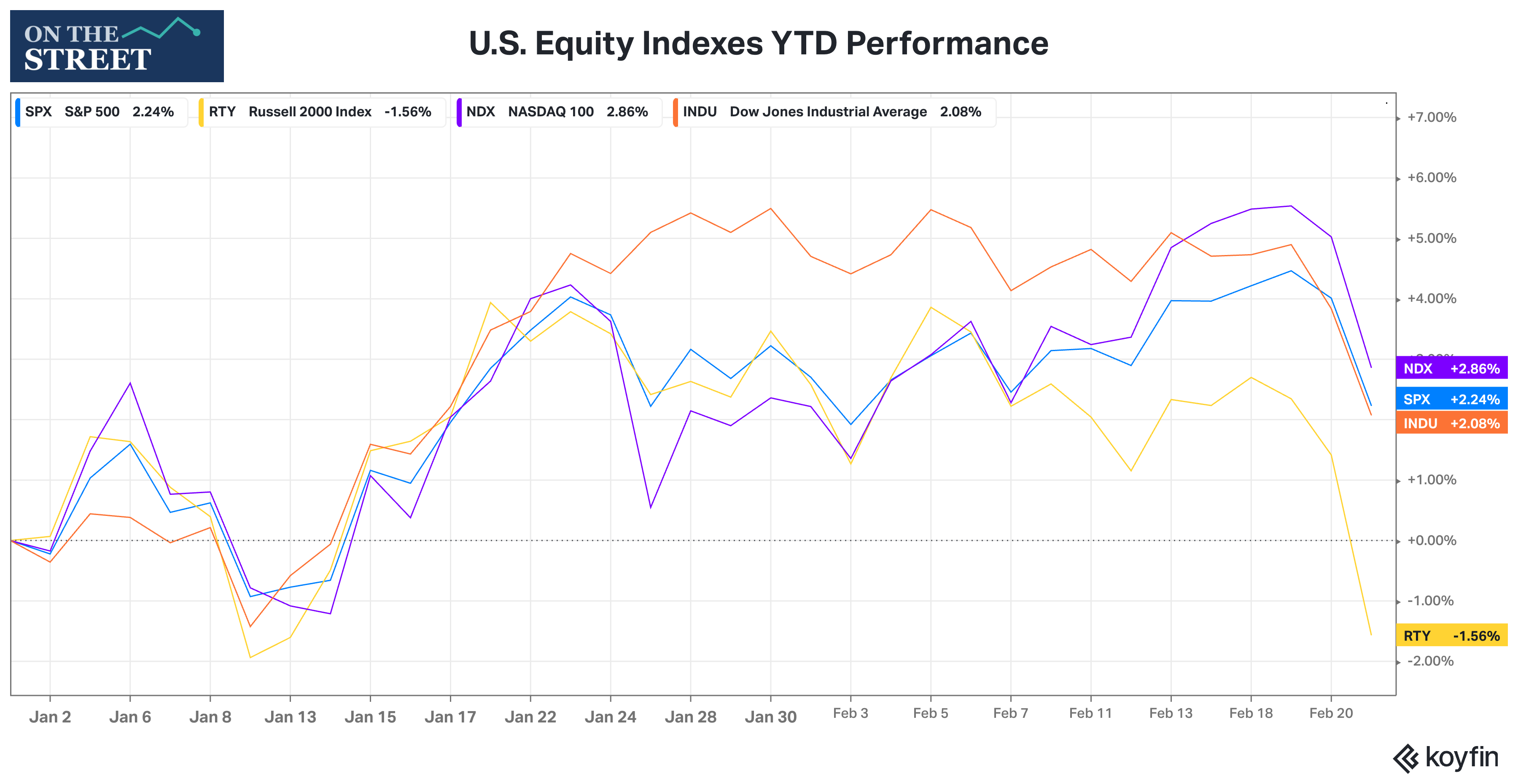

Year-to-Date in the U.S., small cap stocks have erased all the gains they made during the year and are down over 1.5% while the S&P 500, Nasdaq-100 and Dow Jones are all up over 2% for the year.

In other parts of the world, stocks have also been performing quite well, despite many risks, not the least of which are trade and geopolitical tensions. The MSCI All Countries World Index is up 5.2% YTD. European markets have also risen quite substantially, with the FTSE 100 up over 6%, and the DAX in Germany up over 11%. Much of the same is happening in Asia and South America as well. Why does that seem to be the case? Well, valuation multiples in American equities have been fairly high recently. The S&P 500 is trading at a trailing twelve month (TTM) P/E ratio of 29. Meanwhile, the MSCI All World Index’s TTM P/E ratio is currently ~24, and the MSCI Europe Index TTM P/E ratio is ~16. Multiples in the U.S. had been expanding for quite some time, thanks to a very strong U.S. economy, technological innovation and growth. It seems like now; however, returns are regressing back to the mean, allowing the rest of the world to catch up a bit. Investors also seem to be signalling that U.S. multiples are a bit on the expensive side – one of the main reasons I have found it difficult to find a high-quality stock, trading at a fair price, to outline in greater detail as of late.

While much of U.S. markets seem like their valuation is on the expensive side right now, there may be potential opportunities beginning to emerge.

Over the past year, the healthcare sector in America, has performed very poorly. XLV, an ETF tracking the sector, is up a mere 2.5% for the year. There are many reasons the healthcare sector has not been a good performer this year, but the main reason is the potential for major health reforms. Just this week, the Wall Street Journal reported that the DoJ began a probe into one of the biggest companies in the sector, UnitedHealth Group Inc., causing their stock to decline over 7% on Friday. Shares of one of the major obesity drug providers, Novo Nordisk, are down over 26% in the past year. Even CVS, a household name in the sector is down 13% over the last year. While there is still lots of uncertainty over what’s going to happen in the short to medium term with this sector, it’s one to keep a close eye on as multiples contract, and as we begin to get a clearer picture of what potential changes the Dept. of Health, led by RFK Jr., will enact.

Another sector that’s been having a rough year is homebuilders. The iShares U.S. Home Construction ETF (ITB) that tracks the industry is down a little over 7% over the last year, due to higher interest rates taking a toll on demand. Valuations have dropped significantly, and this is an industry to keep a close eye on should inflation recede, and we get some more rate cuts. For the time being, however, its one to generally avoid, given the fact that demand is facing some headwinds.

Mega-Cap tech stocks have also taken a bit of a beating this month. Google now trades at an historically low valuation – a price of 22x earnings for the last twelve months. Meta has also fallen every day over the last week and trades at a PE of 28. Amazon has also fallen 12.14% since February 4th, and trades at a price to earnings multiple of 38.5. With the EU reassessing tech probes into some of the largest US tech companies, investors seem to be taking some of the gains in those stocks. Names like Google are looking more attractive at this price, while risks still remain. The biggest risk to Google’s business is the entrance of AI chatbots which do a lot of what Google search has done and, in some ways, do it a bit better. Google’s CEO has said that their search engine will change profoundly in 2025, probably in an effort to keep up with AI chatbots like Perplexity, ChatGPT and Claude. Their brand still has a ton of value, even though competition has become incredibly more fierce. This is a company I will be paying close attention to this year.

The U.S. agricultural industry has also had quite a tough past few years. The price of eggs has risen by around 15% this year, as the bird flu takes a toll on the chicken and egg industry. The population of egg-laying hens has fallen by over 10% in the past few years due to the flu, and officials are looking for a solution. Zoetis Inc., a company focused on animal health and medicine just received conditional approval for their bird flu vaccine in poultry, but there are still some hurdles the industry will need to go through before chickens get vaccinated. Governments that import U.S. poultry products will need to accept imports that have been vaccinated, which could take some time. One of the largest U.S. producers of eggs, Cal-Maine Foods, has seen the price of its stock decline by over 21% this month.

Finally, I thought that I would look back and reflect on the stocks that I highlighted in my previous newsletters, and how they performed relative to a major benchmark (S&P 500) over the period since I highlighted them. For newsletter issues where I highlighted multiple stocks, I created an equal-weighted “index” to calculate returns and showed the average of the returns of the individual stocks as the equal-weighted return. In the bottom row, I calculated the performance of that average relative to the S&P 500 benchmark.